COVID-19’s impact on beauty retail: how shaken is the beauty industry these days?

When we sit in our homes all day, on Zoom calls without sharing the camera, or go out with just mascara on, it seems natural that the investment in beauty products is lower. But just how low and for how long? How has the pandemic shaken down the beauty industry and how can retailers and brands adapt to get through this period?

This article assesses the beauty industry’s short- and medium-term impact, drawing on multiple market reports (McKinsey Consumer Sentiment Survey, Mintel Beauty Trends 2030, Retail Zoom) and official statements from market leaders. When we talk about the beauty industry, we consider the categories of makeup, fragrance, personal hygiene and skin, hair, and body care.

A resilient industry or The Lipstick Index

In the 2008 recession, the market briefly declined and recovered by 2010. And now things seem to be on a similar trajectory. In China, in February, the industry plummeted 80% (year on year), but in March, the decline was 20%. This depreciation does not apply homogeneously to all categories, nor all brands, as we shall see further on.

The beauty industry seems to be very resilient. This can be explained by its rapid dynamics, high level of innovation, digitalization, and efficient use of social media. But in addition to this, we see a specific consumer behavior, for which we use the term Lipstick Index, used in 2001 by Estee Lauder’s chairman.

The Lipstick Index describes people’s motivation to buy small things in difficult times that bring them joy and that they perceive as affordable luxuries – like lipstick. It is one of the plausible explanations why, when a recession, the beauty industry can recover quickly without suffering as big of a loss as related industries, such as fashion.

Revenues in the beauty industry will decline this year by 20-30%, expecting a rebound to the upside in Q1 of 2021, according to McKinsey data.

Online doesn’t make up for sales in physical stores

In the beauty industry, physical space affects 85% of sales, with variations across different categories and consumer demographics. Even Gen Z buys about 60% of beauty products directly from stores. And it is precisely this area that has suffered during the quarantine period. Here is the evolution of the main channels:

Online sales

Against this backdrop, McKinsey expects online sales to grow by 20-30%, a good development, but one that cannot compensate for the volume lost in physical stores. The situation in Romania is similar (according to an iVox study), with a 14.6% increase in online sales in the cosmetics category. Further, 34% of the survey participants declare their intention to continue online purchases in this segment.

Hypermarkets

This is not to say that all categories were in decline, on the contrary. Retail Zoom data shows large increases in hypermarket sales of personal care products in categories such as shampoo, soap, deodorants, facial cleansers, and cotton pads, with increases fluctuating by period but consistently in double digits.

Specialty stores

Sales in specialty stores, mostly located in malls, have suffered a dramatic decline and we expect them to be the last to recover. The major impact can also be seen in the case of Sephora, which in the US decided to lay off 3,754 employees (mostly part-time or seasonal). If we look at China, shopping malls reopened on the 13th of March, and a short period of “revenge shopping” followed, a shopping fever driven by the joy of being able to get out of the house. But traffic in stores remains low and consumers are cautious. 60% of malls reported a 20 to 70% YOY drop in traffic.

The big winner: soap

Working from home, wearing a mask, social distancing, reduced income – all of these cause make-up and perfume to lose relevance, and studies show drops of 55-75%. As wearing a mask will be mandatory indoors, skincare products such as foundation, blush, and highlighter will no longer make sense and the winning products will be those with high transfer resistance. The exception may come from “over the mask” makeup – eye makeup. Amazon reported a 150% increase for this category.

Another category that is proving resilient is self-care & pampering products – for both skin, hair, body, and bath products.

For example, in France, sales of luxury soaps have increased by 800%. Zalando, Europe’s largest beauty industry marketplace, saw increases of up to 300% in candle, aromatherapy, detox, nail, hair, and bath care products. The same categories are also winning on Amazon, where bath products are up 65%, hair coloring 172%, and nail care 218%.

Another trend is the do-it-yourself one, caused by the impossibility of going to beauty salons. Once they reopen, it is expected that some consumers will not resume their habits or will reduce their frequency or consumption. This is why this category (hair dye, specialized skincare products such as masks, nail products) has seen increases of between 23 and 166% in online sales.

In physical stores, the spectacular increases are rather in the care and hygiene categories, such as increases in soap, disinfectant gel, and wet wipes, which have increased in Romania by 3 to 7 times compared to the same period last year.

L’Oreal’s leadership evolution – growth in China and e-commerce

L’Oreal’s Q1 report shows sales down 4.8% globally. The strongest decline is in the Western European market, down 7.7%, while in Eastern Europe the decline was more moderate at minus 1.4% – here we are likely to see a wider decline in Q2. In North America, the decline was 4.8%. One spectacular result is the positive outturn in China, where the company recorded Q1 growth of 6.4%, indicating a trend of market recovery and consumer interest in this product category.

If we look at the category level, the most affected were the luxury (minus 9.3%) and professional (10.5%) ranges, while in the other categories, the average decrease was minus 3.6%. Although the make-up segment is the most affected, hair and skincare products increased, as did hygiene products. In this dynamic, the brands that benefited were Garnier and Dermato-Cosmetics (especially La Roche Posay and CeraVe), the latter generating a 13.2% YOY increase.

Company representatives say e-commerce was key to this growth. L’Oreal’s online sales are up 52.6% year-on-year, already accounting for 20% of the group’s global sales.

It’s clear that this pandemic has accelerated the digital transformation of the beauty industry, and L’Oreal appears to be emerging as a winner, thanks to its mix of e-commerce, digital media, content, trial apps, and other services that deliver a consumer-valued experience.

Jean-Paul Agon, CEO & Chairman of the group, announced a positive development in China, for April the growth estimate is between 5-10%, and for Q2 overall expectations are for double-digit growth.

Europe’s short-term estimates

In Europe, people’s sentiments are rather pessimistic, the main concern coming from the economic situation. According to the McKinsey Global Survey of Consumer Sentiment, the majority of Europeans see the situation in the coming months as uncertain, they expect that the economy will recover in 6 to 12 months. Residents of countries hit hard by the Covid-19 virus, such as Spain, France, and the UK, are even more skeptical, with 40% and 55% expecting a lasting impact of the recession and difficult recovery.

In this context, most say they will cut back on spending in multiple non-essential areas. Expected decreases are higher in skincare and make-up and lower in the personal care segment.

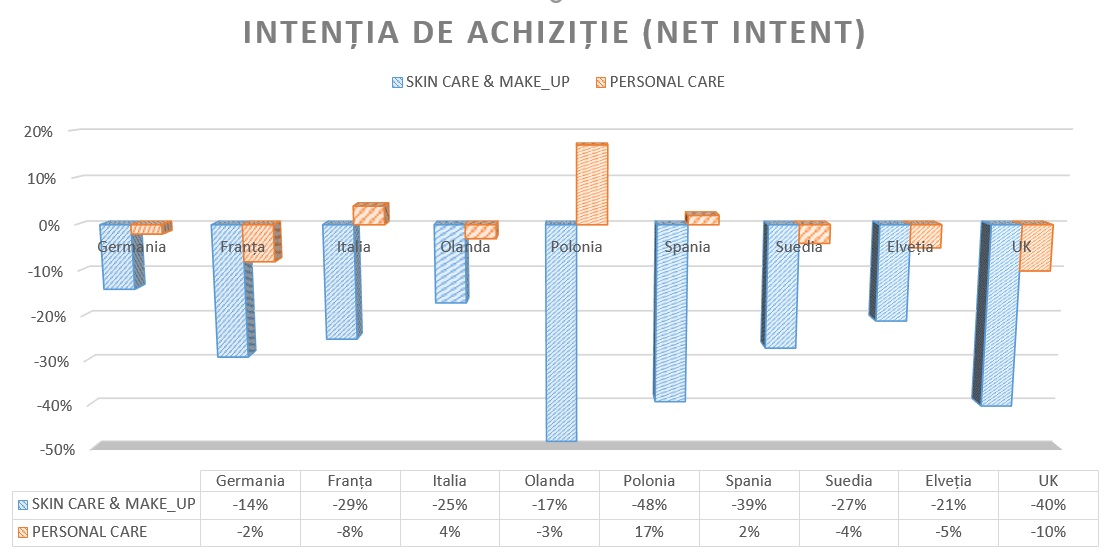

Here are some country-specific data on purchase intentions in the coming period. (Indicators are for net intent – the difference between the percentage of consumers intending to decrease consumption and those intending to increase it).

In terms of trends, consumers say they intend to reduce their purchases of skincare and make-up products by an average of 29% – with Germans estimating the lowest percentage at just 14%, and Poles and people in the UK estimating as much as half the pre-pandemic volume.

For personal care products, we see an intention to maintain current spending (minus 1% on average), with the Poles even estimating over-consumption of plus 17%, but most Europeans are only aiming for a moderate decrease of 2-5%.

Article written by Ioana Mucenic, founder and CEO Minio Studio, for the #retailAboveCorona campaign through which retail.ro aims to highlight the transformations the retail industry is going through, but also solutions, strategies, and opportunities for players affected by the COVID-19 epidemic. For marketing, communication, and service design services, please contact Ioana Mucenic – ioana.mucenic@minio.ro.

Photo source: triocean/Shutterstock

Source: Retail.ro